Bad Credit Score? Here’s How to Still Get Your Mortgage

The surprising truth about mortgage credit scores is that lenders don't require a specific number. In stark comparison to this popular belief, there isn't a universal minimum score needed to qualify for a mortgage.

Lenders use a points-based system that tallies different facts about you at the time you apply for a mortgage. A higher score typically indicates lower risk and increases your chances of approval with better interest rates. Your application might succeed with one lender but fail with another because each uses different scoring systems.

We can help if you’re worried about your credit score’s effect on your mortgage application. Our site offers quick rate and payment estimates, and you can book a call with our mortgage experts on 03330 90 60 30. Check My File provides a 7-day free trial to check your credit score: https://tinyurl.com/3pynuhkv.

In this piece, we’ll explain how mortgage lenders evaluate your application, what affects your credit score, and how you can secure a mortgage even with bad credit.

How lenders assess your mortgage application

Mortgage lenders look at way beyond the reach and influence of your credit report to decide whether they should approve your application. Learning about their assessment process can substantially improve your chances of getting a home loan, even with a less-than-perfect credit history.

What lenders look for beyond your credit score

Credit scores matter, but lenders get into multiple aspects of your financial profile. They inspect your payment history to see if you’ve consistently met your financial obligations on time. Your income level, job stability, and existing debts also play a vital role.

Most lenders give loans of four to five times your salary, though this changes based on personal circumstances. A stable job suggests reliable income, making it attractive to lenders. PAYE employees need to provide recent payslips, bank statements, and their P60. Self-employed people need more documentation, usually two or more years of accounts.

Your debt-to-income ratio (DTI) is vital. This percentage shows how much of your monthly income pays for debt. Most lenders want a DTI under 43%, while some cap it at 36%. A high ratio suggests you might struggle with more debt, whatever your credit score.

A bigger deposit can make a real difference to your application. It reduces the loan-to-value (LTV) ratio, cuts the lender’s risk and might balance out concerns about your credit history.

How affordability checks work

Affordability assessments show how much you can actually borrow. These complete checks look at both income and outgoings to make sure you can handle mortgage payments now and later.

Lenders look at these income sources:

- Regular salary

- Bonuses and overtime

- Income from investments or rental properties

- Benefits and other reliable income sources

They also check these expenses:

- Essential bills like council tax and utilities

- Childcare costs

- Existing debt repayments

- Regular spending patterns

Most lenders ask for three to six months of bank statements to study your money habits. Red flags like gambling or large unusual payments might suggest financial instability.

Stress testing has become standard practise. Lenders run scenarios to see how you’d handle repayments if interest rates went up or your situation changed. This protects both you and the lender from future money problems.

Why different lenders have different criteria

No two lenders use similar assessment criteria. You might get approved by one but turned down by another. Each has its own risk appetite and internal policies about lending.

Some lenders work specifically with people who have less-than-perfect credit histories. These specialist lenders take an all-encompassing approach to your finances and look beyond credit scores to see your full financial picture.

Lenders also treat income types differently. To name just one example, some count pension contributions as deductions while others don’t. The way they calculate overtime, commission, and bonuses varies substantially between lenders.

You should check your credit score with a 7-day free trial at Check My File (https://tinyurl.com/3pynuhkv) before applying. This shows you what lenders will see when they review your application. To get personalised advice about suitable lenders, you can get a quick rate and payment estimate on our site or call our mortgage experts at 03330 90 60 30.

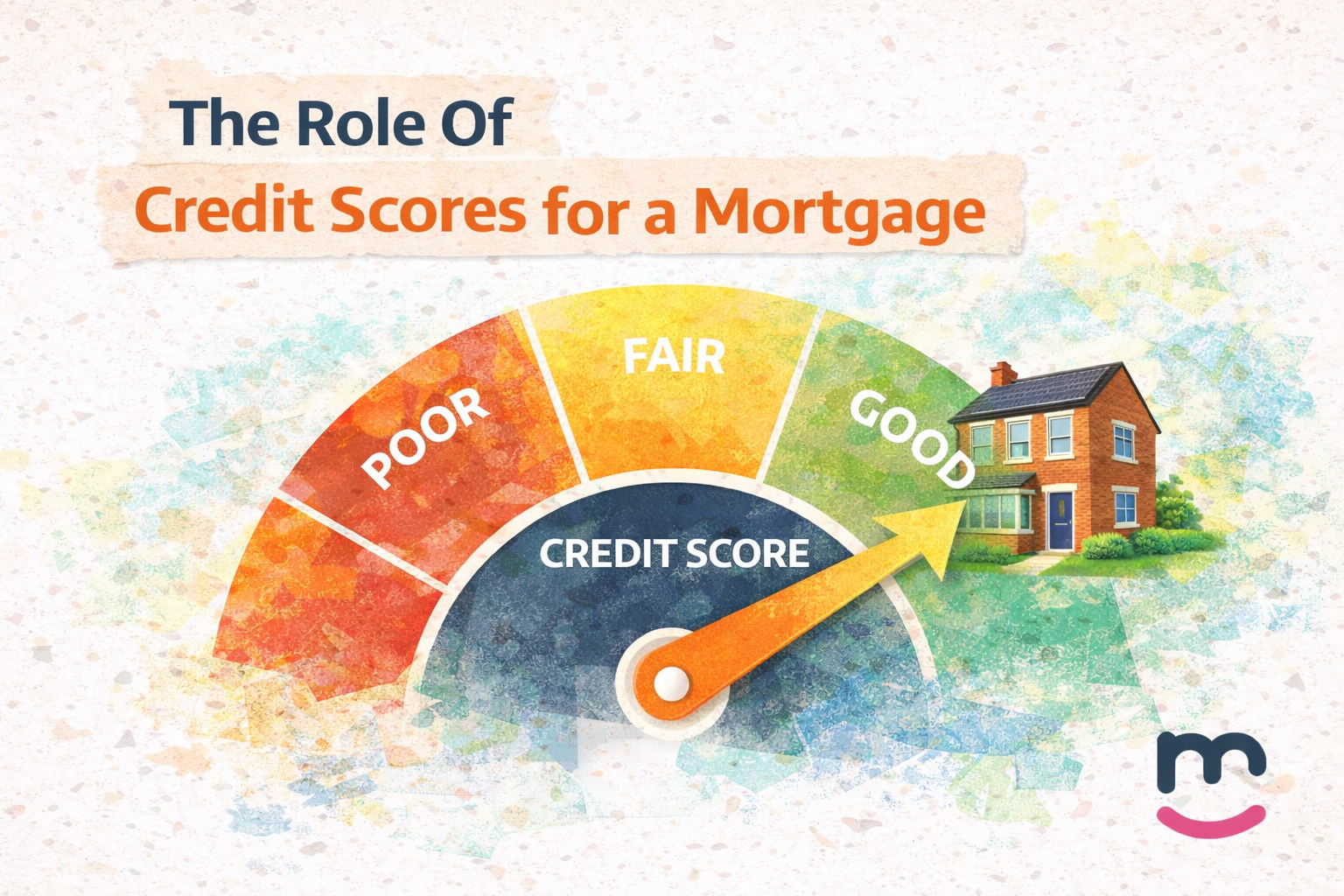

What credit score is needed to buy a house?

The magic number needed to get a mortgage is a question that keeps many homebuyers up at night. You might expect a simple answer, but it’s not that straightforward. Let’s break down how credit scores affect your chances of getting a mortgage in the UK.

Understanding credit score ranges

The UK has three main credit reference agencies that calculate your credit score. Each agency uses its own scale:

- Experian: Scores range from 0–999, with 881+ considered good

- Equifax: Scores range from 0–1000 (previously 0-700), with 420+ considered good

- TransUnion: Scores range from 0–710, with 604+ considered good

Each agency has its own way of categorising scores, but they share similar classifications:

- Excellent: Best mortgage options with lowest interest rates

- Good: Most mortgage products available with competitive rates

- Fair: Some limitations with potentially higher rates

- Poor: Limited lenders and stricter conditions

- Very Poor: May require specialist lenders

A score above 800 with Experian or Equifax, or above 700 with TransUnion puts you in a great position. Scores between 600-799 can still get you a mortgage, though lenders might be more careful.

How your score affects mortgage rates

Your credit score directly influences both your approval chances and borrowing costs. A small change in interest rates can make a big difference to your monthly payments and the total cost of your mortgage.

Here’s the reality: better credit scores mean better interest rates. A borrower with an excellent score could get an interest rate 0.6% lower than someone with a fair score. This small difference could save you thousands over your mortgage term.

Your credit score also affects:

- The size of deposit required

- Loan limits you qualify for

- Your acceptable debt-to-income ratio

- Application fees

A higher credit score makes the mortgage process easier and cheaper.

Why there’s no universal minimum score

Most people believe there’s a minimum credit score needed for a UK mortgage. In stark comparison to this belief, each lender sets their own criteria based on their risk appetite and business model.

Here are some important points:

- Lenders create their own internal scoring systems using information from credit reference agencies

- The same person might get approved by one lender but rejected by another

- Some specialist lenders skip credit scoring systems and review applications case-by-case

Most conventional loans need scores around 620+. FHA loans might accept scores as low as 500 (with a 10% deposit) or 580 (with 3.5% down). VA loans don’t have minimum score requirements, but individual lenders often set their own limits.

Not sure about your score? Check My File offers a 7-day free trial at https://tinyurl.com/3pynuhkv. This shows you what lenders see when they review your application.

Need personalised advice about your mortgage options? Get a quick rate and payment estimate on our site or call our mortgage experts at 03330 90 60 30 for guidance tailored to your situation.

Can you get a mortgage with bad credit?

You might be surprised to learn that bad credit doesn’t automatically rule out your chances of getting a mortgage. The path to homeownership exists even with a flawed credit history, though you’ll face more obstacles along the way.

Types of bad credit that affect your chances

Your mortgage application faces different challenges based on your credit problems and when they occurred:

- Missed payments on bills or debts are relatively minor problems, especially when they happen once in a while

- Defaults happen when you stop making payments and the lender stops trying to collect normally

- County Court Judgments (CCJs) stay on your record for six years, though some lenders look at applications after three years if you’ve paid your debts

- Individual Voluntary Arrangements (IVAs) usually mean waiting up to six years before you can apply

- Bankruptcy usually needs six years to pass since discharge before mainstream lenders will think about your application

- Debt Management Plans (DMPs) aren’t as serious but still show you’ve had money troubles

Timing plays a vital role. Recent financial troubles mean you’ll need bigger deposits than if they happened years ago. Most lenders care more about your recent money management than old problems.

How much deposit you might need

The worse your credit issues, the bigger deposit you’ll need:

- Minor issues like late payments need 5-10%

- Defaults or CCJs require 10-15%

- Debt management plans usually need 15-30%

- IVAs typically call for 25-30% deposits

- After bankruptcy or repossession, you’ll need 30-40%

- Multiple credit problems might require 30-40% or more

A bigger deposit helps your chances by a lot because it reduces the lender’s risk.

Specialist lenders for poor credit applicants

Good news – some lenders specialise in helping people with troubled credit histories:

- Pepper Money has flexible rules for people with financial difficulties

- Bluestone Mortgages looks at each case individually instead of using automated systems

- Vida Homeloans believes everyone deserves another chance and doesn’t just look at credit scores

- Kensington Mortgages uses experienced staff to handle complex cases

These lenders charge higher interest rates to balance their risk. They are a great way to get approved when regular banks say no.

Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv to see what lenders will find. Our experts can help you find lenders who might work with your situation – get a quick rate and payment estimate on our site or call us at 03330 90 60 30.

How to improve your credit score before applying

You need time to boost your credit score, but several practical steps can improve your rating before you submit a mortgage application. A few small improvements will make a big difference to your available rates and products.

Make payments on time

Your credit score and mortgage eligibility depend heavily on timely payments. A single missed payment can hurt your score and stay on your credit report for six years. Direct debits will automatically pay your bills and help you avoid late payments. You should set up automatic payments that cover the minimum amount due each month for your existing credit accounts. Many creditors will work with you to create manageable payment plans if you reach out to them quickly about payment difficulties.

Register on the electoral roll

Your credit score could jump up to 50 points just by appearing on the electoral roll. The surprising fact is that all but one of these people know about this effect. Lenders can confirm your identity and address faster through your registration, which speeds up credit applications. The online registration process takes just minutes and it’s a legal requirement anyway. You can register at your current address whether you live in shared accommodation or with parents.

Avoid multiple credit applications

Your score drops substantially when you apply for multiple credit products in a short time lower your score. Lenders see every hard search that each application triggers on your credit report. The best approach is to space out your applications – aim for no more than one every three months. Smart mortgage applicants use eligibility checkers first because these run soft searches that don’t hurt your score.

Check for errors on your credit report

Declined applications and lower scores can result from small mistakes like a mistyped address. Regular reviews of your credit report help you spot errors or outdated information. The credit reference agency or provider should be contacted directly if you find inaccuracies. Special circumstances behind negative marks can be explained through a “Notice of Correction”.

Use a credit builder card wisely

People who haven’t borrowed before can establish a positive payment history with credit builder cards. These cards work best for small, regular purchases that fit your budget. Interest charges can be avoided by paying the full balance monthly. The card might briefly lower your score at first, but responsible use typically raises it within about six months.

Before applying for a mortgage, check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv. Our site offers quick rate estimates based on your current credit situation, or you can call our experts directly at 03330 90 60 30.

Tools and expert help to boost your chances

You can boost your chances of mortgage approval by getting expert help and using the right tools, even with credit issues. Let me show you how to get the support you need during this process.

Check your credit score with a 7-day free trial at Check My File

You need to know exactly what lenders see before you apply for a mortgage. Most brokers use soft search credit checks from major credit reference agencies to find issues that affect your score. Looking at your credit report early helps you spot potential red flags that might worry lenders. It also lets you find and fix any mistakes that could hurt your application.

Check My File’s 7-day free trial gives you the complete picture: https://tinyurl.com/3pynuhkv. You’ll see data from multiple credit agencies in one place, giving you a full view of your credit standing.

Get a quick rate and payment estimate on our site

Understanding your credit position helps you get realistic mortgage estimates. Our online calculators help you see likely monthly payments for different mortgage deals. This gives you clear expectations about what you can afford before talking to lenders.

Call our mortgage experts directly at 03330 90 60 30

Bad credit applications have better success rates with specialist brokers. Research shows more than 15 million people in the UK have adverse credit histories. Our advisors look at your credit reports, help you build better credit, and find lenders who are likely to approve your situation.

Specialists know which lenders match your specific needs, which helps avoid rejected applications that could damage your credit score further.

Conclusion

Getting a mortgage with less-than-perfect credit is challenging. You can still make it happen with the right approach, despite what many think. Most homebuyers believe they need a specific credit score to get approved. Lenders look at your complete financial picture rather than just one number.

Your success depends on how different lenders look at applications. Each lender has their own criteria, so a rejection from one doesn’t mean others will say no too. Specialist lenders provide good options if you have credit issues, but they usually charge higher interest rates.

Your credit problems’ age and seriousness affect your approval odds and deposit needs by a lot. Taking steps to boost your score before applying can open up more options. Regular payments, getting on the electoral roll, and smart credit card use will help improve your score.

Expert guidance is your best tool when applying for a mortgage with bad credit. We match you with lenders who are more likely to approve your situation. This helps you avoid rejected applications that could hurt your score even more.

Check your credit score before you start your mortgage hunt. You can get a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv. This shows you what lenders see when they review your application. You can also get quick rate and payment estimates on our site. Our mortgage experts are available at 03330 90 60 30.

Past money troubles don’t mean you can’t own a home. Good preparation, expert help, and staying determined will help you get the mortgage you need to buy your home.

Key Takeaways

Getting a mortgage with bad credit is challenging but entirely achievable with the right strategy and expert guidance.

- No universal minimum credit score exists – lenders use different criteria, so rejection from one doesn’t mean rejection from all

- Larger deposits offset credit issues – expect 10-40% deposits depending on severity, with recent problems requiring more than historical ones

- Specialist lenders cater to bad credit applicants – they assess cases individually rather than relying solely on automated scoring systems

- Simple credit improvements deliver big results – electoral roll registration can add 50 points, whilst timely payments prevent six-year damage

- Professional guidance prevents costly mistakes – mortgage brokers identify suitable lenders and avoid rejected applications that further harm your score

The key is understanding that lenders evaluate your complete financial picture, not just your credit score. With proper preparation and specialist support, homeownership remains within reach despite past financial difficulties.