Why Most First-Time Buy to Let Mortgage Applications Fail (And How to Succeed)

Thinking about your first buy to let mortgage? Here's the reality: most applications get rejected before they even reach an underwriter.

Why do so many fail? Simple. First-time landlords don’t understand what lenders actually want. You’ll need at least a 25% deposit – sometimes up to 40%. Your rental income must cover 125% to 145% of mortgage payments. Plus, buy to let mortgages carry higher rates and stricter criteria than residential deals [-5].

Sounds daunting? Here’s better news. Annual buy-to-let costs have dropped 24.6% year-on-year. More importantly, you can dramatically improve your approval chances with the right preparation.

What you’ll discover:

- The six reasons applications fail

- Exactly what lenders look for

- How to position yourself for success

Ready to get started? Get quick rate quotes on our site or book a call with our experts on 03330 90 60 30. Before you apply anywhere, check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv.

Why most first-time buy-to-let mortgage applications fail

Lenders reject applications for very specific reasons. Understand these six failure points and you’ll avoid the most common mistakes.

1. Poor credit history or low credit score

Your credit history matters more than you think. Even small credit hiccups can sink your application entirely. Some lenders won’t touch anyone with adverse credit history. Others specialise in bad credit cases – but expect higher rates.

Lenders calculate your score using your credit report, application details, and their own records. Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv.

2. Insufficient deposit or savings

Here’s what most first-time landlords get wrong: they save the minimum and wonder why they get rejected.

You need at least 25% deposit for most buy to let mortgages. Some lenders want up to 40% for certain properties. Yes, a few offer 15% deals – but they’re rare and expensive.

Smaller deposits mean higher rates and negative equity risk when markets drop. Save more. Get better rates. Reduce rejection risk.

3. Unrealistic rental income expectations

Lenders expect rental income to cover 125-145% of your monthly mortgage payments. This Interest Coverage Ratio (ICR) protects against void periods and unexpected costs.

Fall short during the valuation? Application rejected. Higher-rate taxpayers face even stricter ratios. Know your numbers before you apply.

4. Incomplete or inaccurate paperwork

This one’s entirely preventable. Yet first-time landlords consistently underestimate the documentation required.

Submit incomplete paperwork? Instant rejection. Portfolio landlords face even stricter requirements. Create a comprehensive checklist. Double-check everything. Avoid this entirely avoidable failure.

5. Choosing the wrong property type

Not every property qualifies for buy to let mortgages. Lenders exclude:

• Properties with planning restrictions • Freehold flats and maisonettes

• Unlicensed HMOs • Properties under £75,000 • Studio flats under 35m²

Standard residential properties get approved easier than holiday lets or commercial conversions. Choose wisely.

6. Not meeting lender income requirements

Buy to let mortgages focus on rental income – but most lenders still want minimum personal income of £25,000-£30,000 annually. This protects them during void periods.

First-time landlords face stricter income criteria than experienced investors. Stable employment or reliable self-employment income becomes crucial.

Need guidance? Book a call with our experts on 03330 90 60 30 or get quick rate quotes on our site.

What Lenders Actually Want From You

Know exactly what you’re up against before you apply. Here’s what lenders check first – and what trips up most first-time landlords.

Your Essential Checklist

Age and Income Requirements Most lenders want applicants aged at least 21, though some accept from 18. You’ll need a minimum annual income around £25,000 plus a clean credit history.

Property Ownership

Some lenders don’t require you to own your residential property. Others insist at least one applicant already owns a UK property.

Property Standards The property must be worth at least £50,000 with a minimum EPC rating of ‘E’ or above.

Property Types Lenders Won’t Touch:

- Multiple tenancy properties

- Homes of Multiple Occupation (HMOs)

- Properties falling under selective licencing schemes

- Holiday homes or lets

Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv.

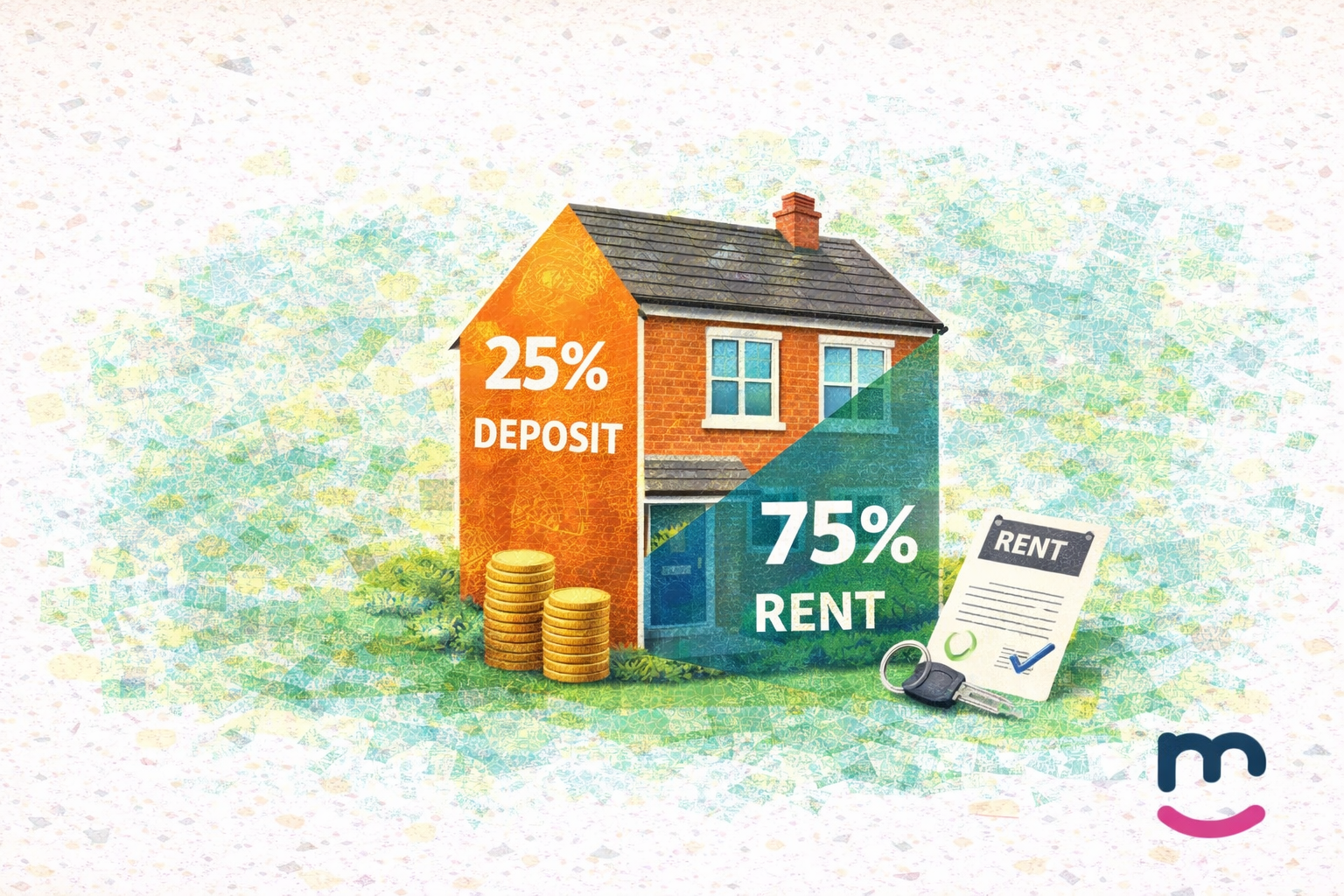

Deposits: More Than You Think

Forget what you’ve heard about 15% deposits – they’re virtually impossible to find. Reality check: most lenders require at least 25% of the property’s value [111]. Some demand up to 40%.

Quick calculation: £250,000 property = £62,500 minimum deposit.

Bigger deposits get you better rates [111] and lower risk. Save more than the minimum if you can.

How Buy to Let Mortgages Work

The Big Difference Residential mortgages focus on your personal income. Buy to let mortgages care about rental income from the property.

Interest-Only Structure Most buy to let mortgages are interest-only. Monthly payments cover just the interest. You repay the loan amount at the end through property sale, savings, or refinancing.

Higher Costs Expect higher interest rates than residential mortgages due to increased lender risk. The application process stays similar, but eligibility criteria are much stricter.

The Rental Income Test

Stress Testing Lenders stress test your ability to pay if rates rise significantly. They use the Interest Coverage Ratio (ICR) – rental income must cover 125% to 145% of monthly mortgage payments.

Tax Status Matters:

- Basic rate taxpayers: 125% ICR

- Higher rate taxpayers: 145% ICR [141]

- Additional rate taxpayers: up to 150% ICR

Real Example £150,000 loan at 5.5% stress rate = £8,250 annual interest. With 125% ICR, you need £10,312.50 yearly rental income (£859 monthly).

Top Slicing Option Some lenders allow you to use surplus personal income if rental income falls slightly short. Particularly useful for first-time landlords in lower-yield areas.

Get personalised advice on our site or book a call with an expert on 03330 90 60 30.

Boost Your Approval Chances

Want to avoid rejection? Here’s exactly what you need to do.

Fix Your Credit Before You Apply

Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv.

Lenders scrutinise every detail of your credit history. One missed payment can kill your application.

Essential steps:

- Check for errors and dispute them immediately

- Pay all bills on time for six months before applying

- Stay within existing credit limits

- Don’t apply for new credit cards or loans

Save More Than the Minimum

Most lenders want 25% deposits, but smart landlords save more. Why? Better rates and lower risk.

High-value properties might demand 40%. Those tempting 15-20% deposit deals? They come with painful rates and fees.

Work With a Specialist Broker

Mortgage brokers know which lenders accept first-time landlords. They have direct relationships with underwriters and can fast-track applications.

More importantly, they understand which products suit your specific situation. This saves you weeks of research and rejection letters.

Pick Properties Lenders Love

Your rental income must cover 125-145% of mortgage payments. Choose wisely.

Properties near transport links generate consistent rental income. Lenders prefer consistency over flashy investments.

Get Your Paperwork Perfect

Incomplete applications get binned immediately. You’ll need:

- Proof of identity and income

- Bank statements showing your deposit

- Details of existing properties

- Expenditure records

Self-employed? Add your latest two years’ tax calculations and year overviews.

Speak To An Expert

Professional guidance can turn rejections into approvals.

Book a call with our specialists on 03330 90 60 30 or get quick rate quotes directly on our site.

Choosing the Right Mortgage Type

Your mortgage choice affects every penny of profit. Pick wrong, and you’ll struggle from day one.

Interest-only vs repayment: pros and cons

Most buy-to-let mortgages work on interest-only terms. You pay just the interest monthly – not the capital borrowed. Lower monthly payments mean better cash flow. But here’s the catch: you still owe the full amount at the end.

Repayment mortgages work differently. Monthly payments cover both interest and capital. Higher monthly costs, yes. But you’ll own the property outright eventually.

Which suits you? Interest-only wins for monthly cash flow. Repayment wins for long-term ownership.

Fixed vs variable rates: what suits first-time landlords?

Fixed-rate mortgages lock your rate for 2-5 years. No surprises. No budgeting headaches. Variable rates move with the market – great when rates fall, painful when they rise.

First-time landlords usually prefer fixed rates. Why? Predictable monthly payments make planning easier. Just remember: fixed rates eventually revert to higher standard variable rates.

Top-slicing and deferred interest options

Rental income falling short by £100-200 monthly? Top-slicing might help. Lenders use your personal income to bridge the gap. Some require minimum personal income of £50,000.

Deferred interest lets you start with lower payments, adding interest to the loan. Helpful short-term. Expensive long-term.

How to get a buy to let mortgage first time buyer

Work with a specialist broker. They know which lenders welcome first-time landlords. Some lenders even accept applications from up to three people, spreading costs and profits.

Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv and get quick rate quotes on our site. For personalised guidance, book a call with an expert on 03330 90 60 30.

Costs and Legal Responsibilities to Prepare For

Got your mortgage approved? That’s just the beginning. First-time landlords face substantial ongoing costs and legal obligations that catch many off guard.

Stamp Duty and Legal Fees

Buy-to-let properties carry a 5% stamp duty surcharge above standard rates. That £200,000 investment property? Expect £11,500 in stamp duty. Legal fees add another £600-£1,500, with leasehold properties costing more.

Letting Agent and Management Costs

Full property management eats 8-20% of monthly rental income. This covers tenant finding, rent collection, maintenance coordination, and compliance management. Even basic tenant-find services can cost one month’s rent.

Void Periods and Maintenance

Empty properties kill profitability. You’ll still pay mortgage, council tax, and utilities with zero rental income. Set aside one month’s rent annually for unexpected repairs.

Landlord Insurance and Safety Certificates

Standard home insurance becomes invalid once you let a property. You’ll need specialist landlord cover plus mandatory certificates:

- Annual gas safety certificates (£60-£90)

- Five-yearly electrical safety checks (EICR)

- Energy Performance Certificates (valid for 10 years)

Tenancy Agreements and Deposit Protection

Proper tenancy agreements protect both parties. Deposits must go into government-approved schemes within 30 days. Miss this deadline and face penalties.

Ready to factor these costs into your investment planning? Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv or call our experts on 03330 90 60 30.

Your Next Steps

Ready to succeed where others fail? You now know exactly why most applications get rejected – and more importantly, how to avoid those mistakes.

The essentials:

- Save at least 25% deposit (more is better)

- Choose properties with strong rental demand

- Get your credit score checked and improved

- Prepare complete, accurate paperwork

- Budget for all additional costs

Remember: buy to let mortgages work differently from residential deals. Lenders focus on rental income, not just your personal income. The rental must cover 125-145% of mortgage payments to pass their stress tests.

Don’t let the additional costs catch you out. Factor in stamp duty surcharges, legal fees, insurance, and potential void periods. You’ll also need annual gas certificates, electrical checks, and proper tenancy agreements.

Ready to get started?

Check your credit score with a 7-day free trial at Check My File: https://tinyurl.com/3pynuhkv.

Get quick rate quotes on our site or book a call with our experts on 03330 90 60 30. We’ll help you find lenders who actually approve first-time landlords and guide you through the entire process.

Your first investment property could be the start of something significant. But only if you prepare properly and get the right guidance from the beginning.

Key Takeaways

Most first-time buy-to-let mortgage applications fail due to preventable mistakes, but understanding lender requirements and proper preparation can dramatically improve your chances of success.

- Save at least 25% deposit – Most lenders require 25-40% deposits, with larger amounts securing better rates and reducing rejection risk.

- Ensure rental income covers 125-145% of mortgage payments – Lenders use stress tests requiring rental income to exceed monthly payments by this margin.

- Check your credit score before applying – Even minor credit issues can derail applications, so review and improve your score beforehand.

- Choose properties with strong rental demand – Standard residential properties in desirable locations with good transport links attract lender approval more easily.

- Budget for substantial additional costs – Factor in 5% stamp duty surcharge, legal fees, insurance, void periods, and ongoing maintenance expenses.

- Use a specialist mortgage broker – Expert guidance helps navigate complex criteria and access lenders more sympathetic to first-time landlords.

Success in buy-to-let investing requires treating it as a business venture with proper financial planning, not just a property purchase. The key is thorough preparation and realistic expectations about both the approval process and ongoing responsibilities.