Green Mortgages: Your Essential Guide to Eco-Friendly Home Financing

Green mortgages are changing the UK housing finance world faster than ever, as 57% of major UK lenders now offer these eco-friendly options - a 4% increase from last year. The market shows greater acceptance of environmentally responsible home financing as a key part of fighting climate change.

The market’s growth is clear – unsecured green home loans have tripled in the last three years, jumping from nine products in 2021 to 27 in 2025. Green mortgages reward homeowners who choose energy-efficient properties or make eco-friendly improvements. These products typically come with lower interest rates and better terms than standard mortgages.

UK buildings contribute about 23% of total greenhouse gas emissions. The Climate Change Committee projects £250 billion in UK home upgrades by 2050. Properties that achieve an A or B energy rating can be worth up to 6% more than those with a D rating. This makes green mortgages a smart choice for both your wallet and the environment.

This piece covers everything about green mortgages and their benefits to your finances and the planet. You can get a quick rate and payment estimate on our site, or book a call with one of our experts at 03330 90 60 30.

What are green mortgages and why do they matter?

Green mortgages work differently from regular home loans. These smart financial products reward homeowners who choose energy-efficient properties or make eco-friendly improvements to their homes.

Definition of green home mortgages

“Energy-efficient mortgages” (EEMs), also known as green mortgages, help people own environmentally friendly homes. Lenders created these special loans to reward buyers who pick energy-efficient properties or upgrade their existing homes to be greener. The term “green” doesn’t mean the money comes from environmental funds – it points to the property’s energy performance.

Lenders might define these loans differently, but they all share one goal: to reward homeowners who choose properties with high energy efficiency ratings. The basic idea stays the same – homeowners get better deals when they support sustainable housing.

How do green mortgages work?

These loans offer three main benefits:

- Preferential rates – Better interest rates on homes with top Energy Performance Certificate (EPC) ratings (A or B)

- Capital release – Money back through credit, lower rates or cashback when you make energy-saving improvements

- Additional borrowing – Extra lending options to buy or refinance homes that need energy upgrades

NatWest gives lower rates on their 2-year and 5-year fixed mortgages if your property has an A or B rating. Nationwide takes it further – they offer 0% interest during the first 2-5 years on extra green borrowing, as long as you spend all the money on things like solar panels, heat pumps, or insulation.

Why energy efficiency is now a financial priority

Money-smart homeowners care about energy efficiency. Energy-efficient upgrades save substantial money over time. Better insulation and modern heating systems cut utility bills enough to cover the extra mortgage costs.

Homes with higher EPC ratings sell for more money too. Buyers in the UK were ready to pay 9-15% extra for efficient homes according to a 2022 survey. This added “green value” protects against future losses as less efficient properties become harder to sell.

Buildings create about one-fifth of the UK’s greenhouse gases, so lenders see energy-efficient properties as safer investments. Green mortgages help everyone win – homeowners save money and lenders support environmental goals.

Want to learn about your green mortgage options? Check our site to get quick rates and payment estimates, or call our experts at 03330 90 60 30.

Key benefits of choosing a green mortgage

Green mortgages give you more than just environmental benefits. Homeowners across the UK find these eco-friendly financial products attractive because they offer real advantages.

Lower interest rates and better terms

Green mortgages come with better interest rates right away. Lenders want to promote energy-efficient homes, so they offer lower rates that make monthly payments easier to handle. Barclays now gives a 2-year term green mortgage at 4.48% for 60% loan-to-value. You can also get cashback rewards when you complete energy-efficient improvements.

Reduced energy bills and long-term savings

New energy-efficient windows, insulation, and heating systems cut utility costs by a lot. Yes, it is true that energy-efficient property upgrades cost more at first, but the money you save over time makes up for this investment. Heat pumps are a great example – they can slash your electricity and heating bills over the years.

Increased property value and market appeal

Energy efficiency does more than save money on bills – it boosts your property’s value. Oxford Economics found that buyers pay 3.4% more for homes with high energy efficiency compared to standard properties. The Office for National Statistics shows that improving an EPC rating from G to A can boost property value up to 14%. Houses with EPC ratings of A or B sell for 10.9% more than similar homes rated D.

Support for government net-zero goals

Green mortgages are a vital part of the government’s sustainability plan. Houses create 15% of UK carbon emissions, and the government wants to make buildings cleaner and greener. These mortgages help homeowners support the national goal of upgrading as many homes as possible to EPC Band C by 2035.

Want to learn more about green mortgage options? Check our site for quick rates and payment estimates, or call our experts at 03330 90 60 30.

Who qualifies and how to apply for a green mortgage

Getting a green mortgage depends on your property’s energy efficiency. Let’s get into everything about the criteria and how to apply.

EPC rating requirements (A to C)

Most lenders want an Energy Performance Certificate rating of A or B for standard green mortgages. While top ratings are the priority for most financial institutions, some accept high-end C ratings or properties you plan to improve. NatWest specifically wants valid EPC documentation with an A or B rating listed on government registers. These certificates stay valid for ten years, so a new assessment after recent improvements could help you get better mortgage options.

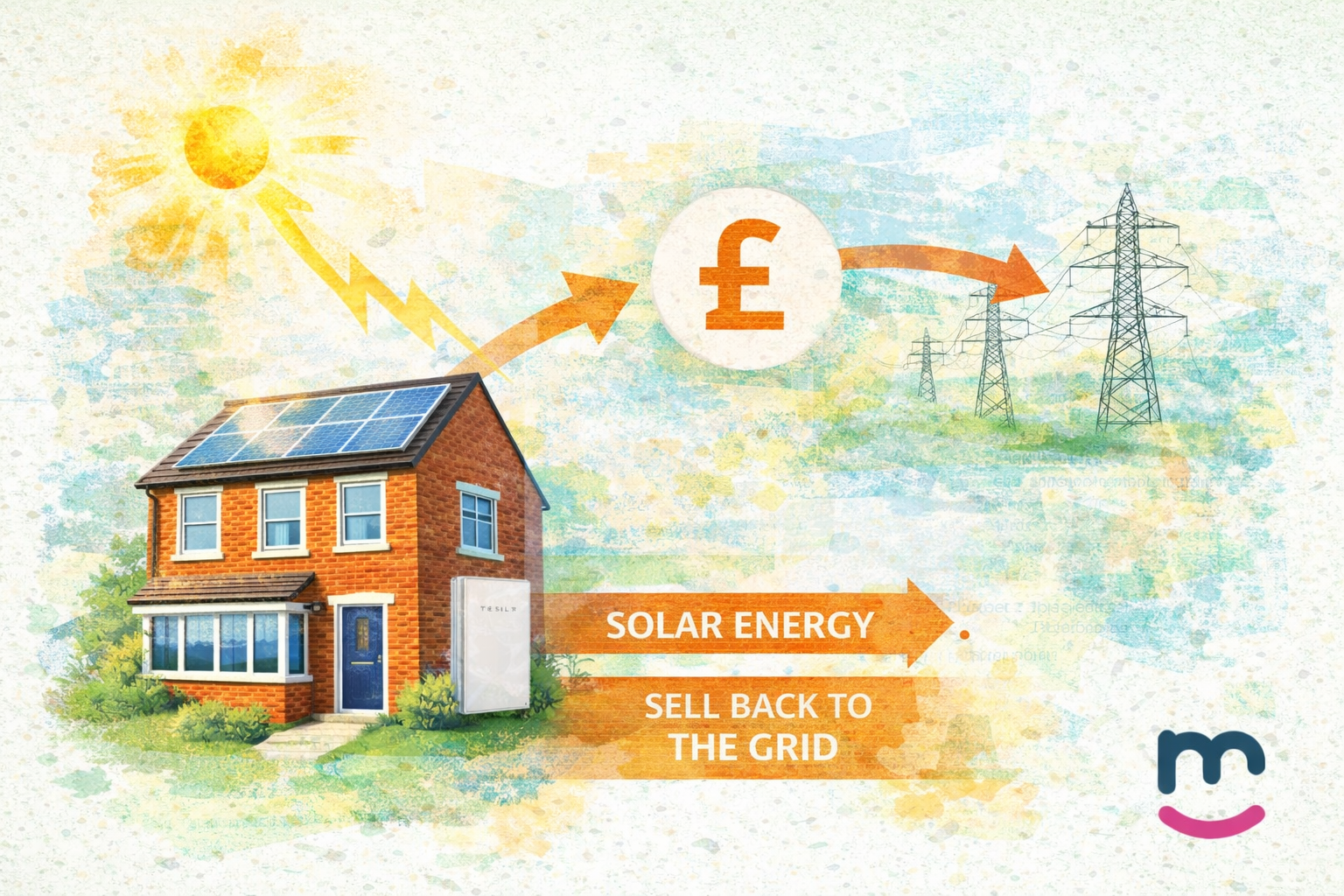

Eligible home improvements (solar, insulation, heat pumps)

When you want funding for eco-upgrades, these improvements usually qualify:

- Solar panels and battery storage

- Heat pumps and boiler upgrades

- Insulation (cavity wall, loft)

- Energy-efficient windows and doors

- Electric vehicle charging points

Some lenders want at least 50% of additional borrowing to go toward energy efficiency improvements. Others like Nationwide require you to use 100% of the money for eligible upgrades.

New purchases vs. refinancing

New builds less than two years old often qualify automatically with lenders like NatWest. Older properties must have documented A-B ratings. Refinancing usually requires existing customers to meet standard lending criteria and complete six consecutive payments. Loan amounts and loan-to-value ratios differ between lenders.

Common lender criteria and documentation

Along with EPC requirements, lenders look at standard factors like income, creditworthiness and loan-to-value ratio. You’ll need valid EPC certificates, original design documents for new builds, and detailed quotes on headed paper for planned improvements.

Want personalised advice? Check our site for quick rates and payment estimates, or call an expert directly at 03330 90 60 30.

The growing market and how lenders are responding

The UK’s green mortgage market has grown faster in recent years. Products have jumped from just 4 in 2019 to over 90 today. This growth shows how consumers want these products and financial institutions are committed to sustainable housing.

Rise in green mortgage products in the UK

UK mortgage providers offering green home finance grew from 38 in 2022 to 39 in early 2023. These providers make up almost 48% of the market. The market now features 76 different green finance options. Research shows half of homeowners and 80% of first-time buyers in Scotland would use these products.

Examples of lenders offering green home finance

Major providers include:

- Barclays, offering discounted rates on properties with energy efficiency ratings of 81+ (bands A or B)

- NatWest, providing reduced rates on 2 and 5-year fixed mortgages for A or B rated properties

- Nationwide, offering cashback of £500 for A-rated properties

Role of the Green Finance Institute and GHFPs

The Green Finance Institute’s Coalition for the Energy Efficiency of Buildings, 4 years old, has shaped the UK market significantly. The Institute launched the Green Home Finance Principles (GHFPs) in 2020. These principles give financial institutions a consistent way to allocate modernisation finance.

Challenges lenders face and how they’re adapting

We have a long way to go, but we can build on this progress. Lenders worry about guaranteeing energy efficiency outcomes and proving “additionality” of lending. The industry tackles these challenges through the Green Home Finance Roadmap. This roadmap focuses on collaborative effort and commercial viability.

You can get a quick rate and payment estimate on our site, or book a call with an expert at 03330 90 60 30.

Conclusion

Green mortgages mark a most important advancement that benefits homeowners and the environment. This piece shows how these innovative financial products reward energy efficiency with better rates, capital release, and many more borrowing options. The green mortgage market has grown remarkably from just 4 products in 2019 to over 90 today. This growth shows how much consumers want these products and lenders’ steadfast dedication to sustainable housing.

Choosing a green mortgage makes sense beyond just helping the environment. Homeowners can get lower interest rates and better terms than standard mortgages. Energy-efficient properties help you save money through reduced utility bills over time. Your property’s value also goes up with high EPC ratings—up to 14% more when improving from a G to an A rating. Smart homeowners see green mortgages as a wise financial move.

These products’ qualification depends on your property’s energy efficiency. Most lenders need an EPC rating of A or B. You can make eligible improvements like installing solar panels, upgrading insulation, adding heat pumps, and fitting energy-efficient windows. Prominent banks like Barclays, NatWest, and Nationwide now provide competitive green finance options. Each lender has different terms and criteria.

This market’s quick growth shows how financial interests line up with environmental responsibility. Buildings create about 23% of total UK greenhouse gas emissions. Green mortgages let homeowners help meet national sustainability goals while saving money.

Want to tap into the potential of green mortgage options for your property? Get a quick rate and payment estimate on our site. You can also book a call with one of our experts at 03330 90 60 30.

Key Takeaways

Green mortgages are transforming UK home financing by rewarding energy efficiency with better rates and terms, whilst supporting environmental goals and delivering long-term financial benefits.

- Green mortgages offer preferential interest rates and cashback for properties with EPC ratings A-C, making eco-friendly homes more affordable to finance.

- Energy-efficient properties command up to 14% higher values and significantly reduce utility bills, creating substantial long-term savings for homeowners.

- The UK green mortgage market has exploded from just 4 products in 2019 to over 90 today, with 57% of major lenders now offering these options.

- Qualifying typically requires EPC ratings A or B, with eligible improvements including solar panels, heat pumps, insulation, and energy-efficient windows.

- Major lenders like Barclays, NatWest, and Nationwide provide competitive green finance options, supporting the government’s net-zero goals whilst benefiting borrowers financially.

With buildings responsible for 23% of UK emissions and the Climate Change Committee projecting £250 billion in home upgrades by 2050, green mortgages represent both environmental necessity and smart financial planning for the future.